For Buyers

The Greater Phoenix housing market remained in a mild buyer's market entering July, with little overall change. The Cromford® Demand Index and Cromford® Supply Index both declined at similar rates over the past 30 days, largely offsetting each other's influence on pricing trends. June closed sales in the Arizona Regional MLS totaled 6,602, up 7.0% from last year, with a 4% increase in sales under $800,000 (equivalent to an extra 221 sales) and a 23% increase in sales over $800,000 (equivalent to an extra 209 sales). Despite stronger sales, prices remained relatively flat below the $1 million price point. Homes priced below $300,000 recorded an average sales price decline of 1.3% compared with last June. Homes priced between $300,000 and $800,000 experienced average price-per-square-foot declines of less than 1%. Meanwhile, homes over $1 million posted modest gains of roughly 1.5% to 2%. This is in stark contrast to recent national headlines stating that home prices set new records in June. If we use the average sales price, then that headline holds true, but the median sales price has not reached a record high and has been stagnant for the last couple of years.

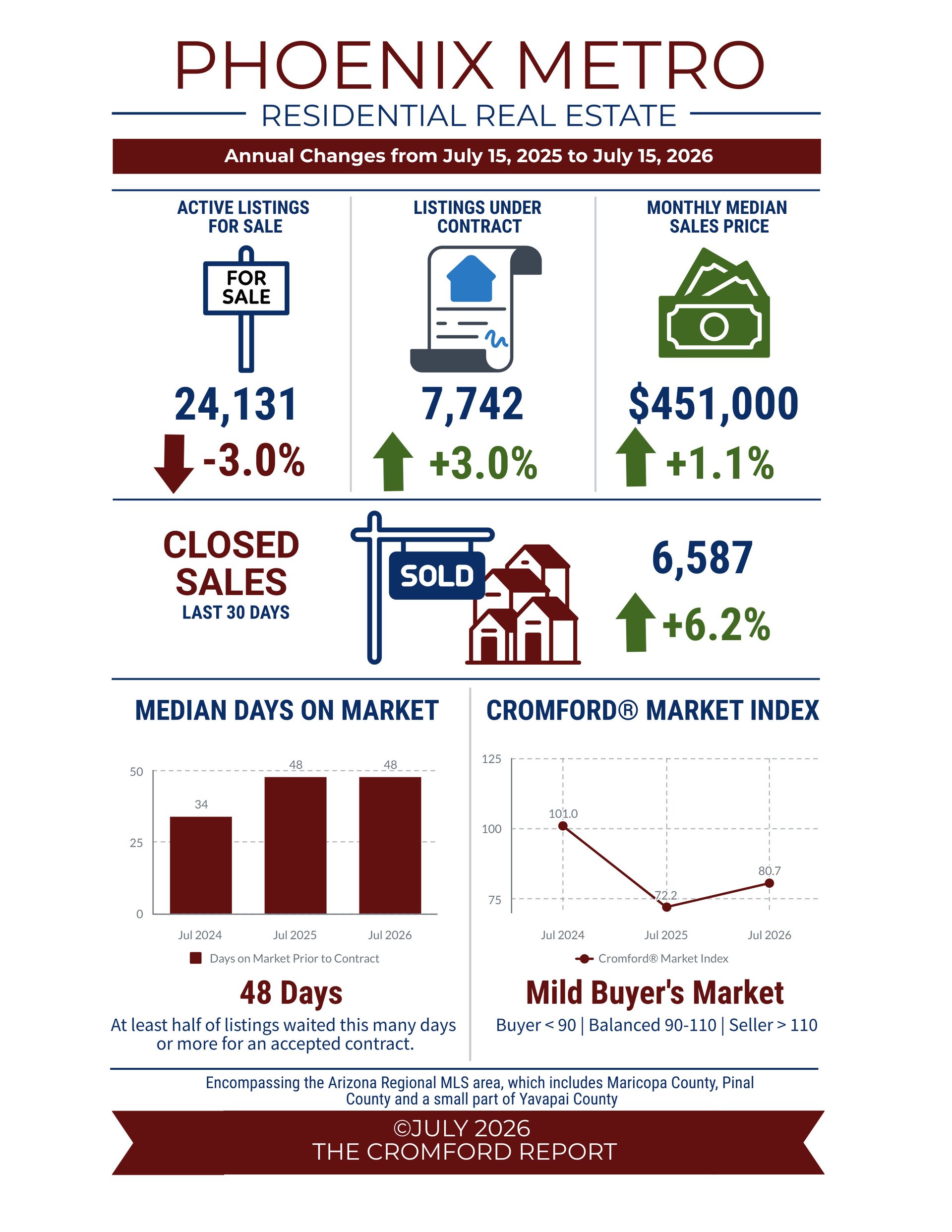

What’s the difference? In the housing market, averages will skew high when luxury sales are strong. For example, the average sales price over the last 30 days in the MLS was $622,000. This can create the impression that the typical buyer is spending that much on a home. In reality, only 27% of buyers purchased homes at or above $622,000, while 73% purchased below that figure.

The median sales price of $451,000 is $171,000 lower than the average. This means half of all buyers purchased a home for $451,000 or less over the past 30 days, making the median a much better representation of the typical transaction. This is also not a record high as it remains nearly $30,000 below the peak median price of $480,000 recorded in May 2022.

Bottom line, don’t assume that home values are currently soaring everywhere, or that luxury sales are causing all home values to rise. It's simply the difference between averages and medians. Historically, home values have not outperformed the rate of inflation in a buyer’s market. In fact, homeowners who purchased within the past 4½ years have generally accumulated little appreciation-based equity. Greater Phoenix income growth, however, has outpaced both inflation and home appreciation for three consecutive years.

For Sellers

Now that the ROAD to Housing Act is law, its effects are unlikely to be felt immediately in the mainstream resale housing market in Greater Phoenix. Most of the changes are structured to reduce construction costs, ease regulations and increase financing options through community banks and updated HUD programs. Other provisions expand grants and forgivable loans for improving aging housing stock, such as aging single family homes owned by low-to-moderate income households. It also prohibits institutions from owning more than 350 homes (with exceptions), which will mitigate risk of future price bubbles but will not have much effect today due to low institutional participation in resale purchases.

As far as spurring new home development in Greater Phoenix, don’t expect it to happen overnight. Builders are painfully aware of what happens when too much supply is added to the market before demand increases. There are other ways to improve affordability without devaluing existing resale homes nearby. To date, new home permits remain 37% below their 2021 peak, in line with the pre-Covid 2019 rate, and total MLS supply is considered normal. The outlying cities where builders operate are in buyer’s markets while established internal cities are in weak-to-moderate seller’s markets. Expect builders to proceed with caution, but with better flexibility to ramp up construction once demand improves.

In the meantime, it’s business as usual for the resale marketplace. The median time on market before contract is 48 days, 55% of closings involved seller-paid closing costs last month, and buyers are negotiating within 97% of list price on average. Condition and competitive pricing are key to keeping marketing times short. The second half of the year is not typically as robust with buyer activity as the first half, so expect marketing times to get a little longer through the remainder of the summer. Lower mortgage rates would certainly boost demand, but sellers should not base their pricing or marketing strategy on that possibility.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

©2026 Cromford Associates LLC and Tamboer Consulting LLC