May Market Update

Conflicting Headlines: Is Supply Too High or Too Low?

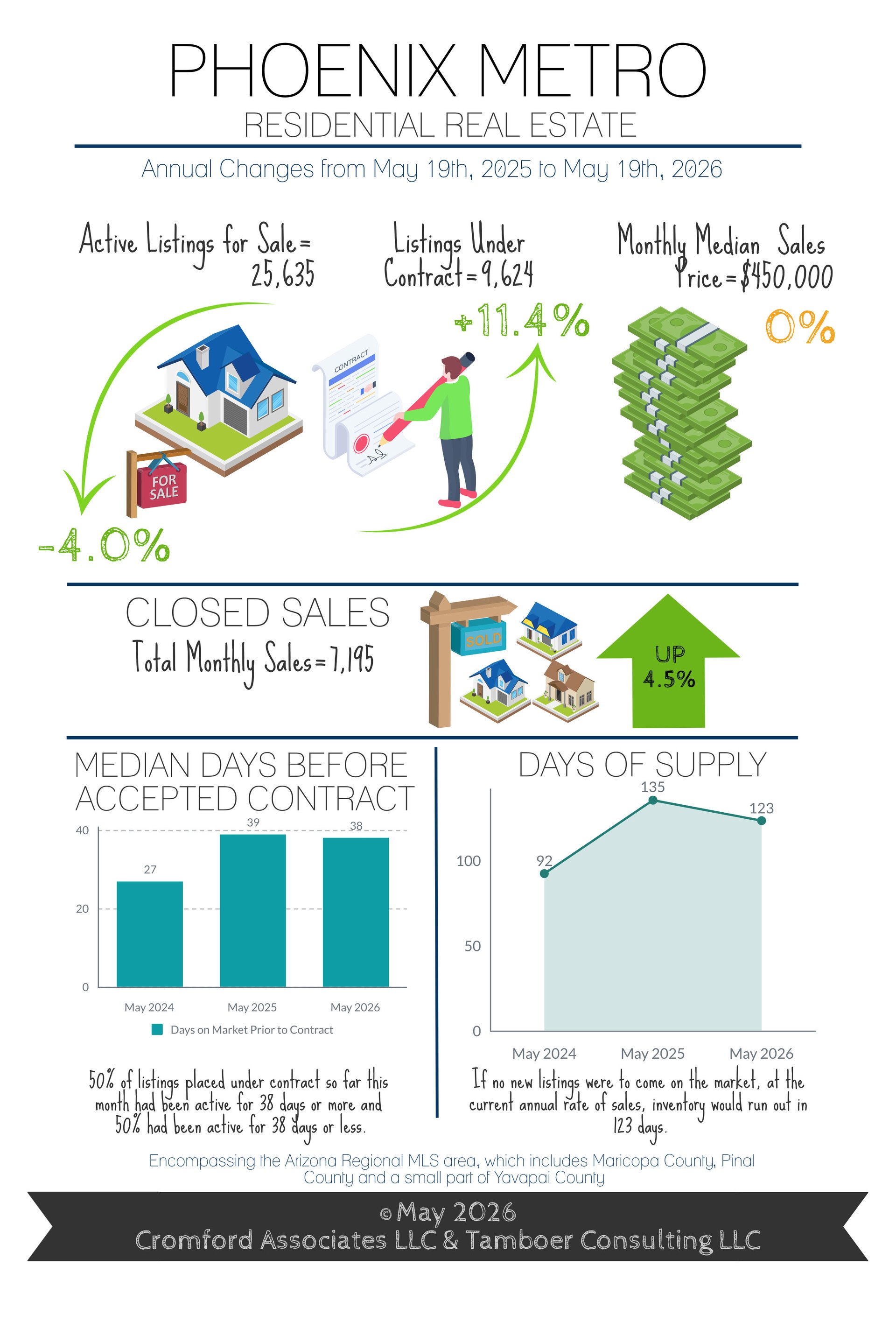

Listings Under Contract Increase 11% in May

Overview

The Phoenix metro market is holding its ground - but it's not uniform, and that distinction matters. Active listings are essentially flat compared to last year, down just 1.1% when you exclude homes already under contract. Monthly sales came in at 7,719, up 5.4% from a year ago, and under contract counts are up 7.7% year-over-year, which signals that demand is real. Pricing held slightly above last year's levels, though when you factor in inflation, median prices and price per square foot are modestly lower in real terms.

The market that exists right now depends heavily on where you're buying or selling, and at what price point.

For Buyers

If you're shopping below $500,000 or looking at condos, townhomes, or apartments, conditions are more in your favor right now. Inventory is higher in those segments and competition is softer. Above $500,000, and especially in central or more desirable locations, you'll find less room to negotiate and homes moving more consistently. The median sales price came in at $450,000, up 1.1% from last year, and price per square foot is at $303.35. Rates remain elevated, but the number of homes going under contract is up meaningfully from a year ago - meaning other buyers are still active. Waiting for conditions to dramatically improve may mean competing with more people when they do.

For Sellers

If you're in a well-located, higher-priced segment - especially single-family detached - the market is still working in your favor. Demand at those price points has held up well and inventory hasn't overwhelmed the market. That said, pricing discipline still matters. April's price per square foot dropped 3.4% from March, and the median price slipped slightly as well. Homes that are priced right are selling. Homes that aren't are sitting, and in a market where active listings are ticking back up month-over-month, sitting is a risk.

Our Take

The headline numbers look reasonably healthy - sales up, contracts up, prices slightly higher than last year. But the story underneath is more nuanced. Demand is concentrated in the right neighborhoods and the right price ranges, and it gets noticeably thinner as you move to the fringes or below $500,000.

The seasonal slowdown that typically arrives at the end of May is coming, so we don't expect dramatic shifts in either direction over the next few weeks. Buyers hold more cards in some parts of the market right now. Sellers hold more in others. Knowing which side of that line your home sits on is exactly where local expertise makes a difference.

©2026 Cromford Associates LLC and Tamboer Consulting LLC